Why in the world would I write about such an esoteric issue as the “Disclaimer Trust?” Simply put, it is one of the best and most frequently used trusts by estate planning attorneys to reduce or eliminate the estate tax and provides great flexibility in your own estate plan. Note, this is not the same thing as a revocable living trust (which I have gently criticized in other articles) because that product is not necessarily an estate tax reduction technique.

Hypothetical scenario: John and Betty have been married for 25 years. They have a house (valued at $400K), a rental (valued at $200k), John’s IRA (valued at $500K), Betty’s IRA (valued at $500K), and a $1M death benefit life insurance policy for a total estate valued at $2.6M.

Issue: Washington State imposes an estate tax on estates valued at over $2,193,000 (inclusive of life insurance death benefit). And, John and Betty have an estate valued at $2.6M.

If John and Betty engage in no estate tax reduction strategy, then they will likely pay the Washington State estate tax. So, how can John and Betty mitigate or eliminate the impact of the Washington State Estate Tax? With the Disclaimer Trust.

Assuming all property is “community property” under Washington law, then we assume that each John and Betty has a one-half interest in the total estate, or $1.3M each. Each is therefore individually under the threshold of the $2.193M established by the state of Washington. But, if John and Betty have a typical estate plan where the survivor inherits everything from the spouse, then the surviving spouse will have an estate valued at $2.6M (now exceeding the threshold amount). There is no tax due upon the surviving spouse’s inheritance, but it inflates the surviving spouse’s estate above the estate tax threshold so that a tax would be due when John and Betty pass all their assets to their two children.

One solution is to provide a mechanism for the surviving spouse to not receive all the assets but to be able to still enjoy the use of the assets.

This usually takes the form of a testamentary trust – a generic term for a trust established in a person’s last will and testament. The Disclaimer Trust is a type of a testamentary trust.

The “Disclaimer Trust” form is particularly attractive because it allows the surviving spouse choice – typically the choice to have a trust or not, the choice of what assets with which to fund the trust, and the choice of how much to put in the trust. The option is exercised by the surviving spouse making a so-called “qualified disclaimer.” A qualified disclaimer is, in simple terms, a directive where the surviving spouse says “I don’t want this asset” and the terms of the will provide that in the event of a disclaimer, the disclaimed asset goes into the trust for the benefit of the surviving spouse.

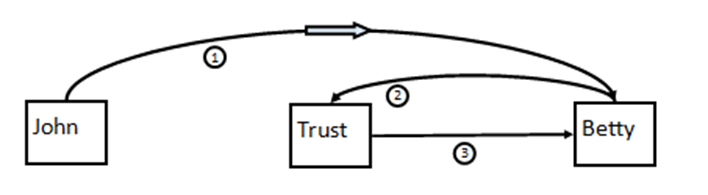

Going back to John and Betty – assume John passes away. Betty could then direct his $1.3 million into a trust for her benefit. She would have her own $1.3M and she would be able to access the other $1.3M held in trust for her benefit (with some restrictions). But her estate would not then be valued at $2.6M because the assets held in the trust don’t count as her assets. Accordingly, her estate is now back under the threshold and all the assets can pass on to the children free of tax.

John and Betty’s Wills facilitate this plan by providing, in general, that all assets go directly to the surviving spouse. But, if the surviving spouse “disclaims” any assets then those assets will be directed to the trust established for the surviving spouse’s benefit. As an example, John’s will would look something like this:

Flexibility: The surviving spouse has the freedom to choose to place assets in the trust or not. Perhaps the surviving spouse doesn’t want to hassle with a trust. He or she need not have a trust. Perhaps the assets have grown and the estate tax burden has likewise grown. The surviving spouse can funnel assets into the trust for protection from the estate tax. Perhaps the assets have diminished, or the estate tax has been abolished – the surviving spouse can choose to have no trust.

If the estate tax is an issue for you and flexibility is important, then the disclaimer trust is a great option. Talk to your estate planning professional to see if the disclaimer trust is right for you.

390757-2

* Licensed, not practicing.

The opinions voiced in this material are for general information only and not intended to provide specific advice or recommendations for any individual or entity. This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Securities offered through LPL Financial, member FINRA/SIPC. Investment advice offered through Cornerstone Wealth Strategies, Inc., a registered investment advisor and separate entity from LPL Financial.